Portfolio Manager Insights | Why Interest Rates Are Defying Expectations Amid Fed Cuts, the Election, and More – 11.6.24

An important yet counterintuitive issue for investors is that long-term interest rates have risen in recent weeks despite the Fed’s latest cuts. The 10-year U.S. Treasury yield, for instance, has jumped from a low of 3.62% to as high as 4.38%. This is due to strong economic data and inflation expectations around the election, both of which push longer-term rates higher. At the same time, rates have swung in either direction for much of the past few years, often without notice. Looking ahead, how might uncertainty around interest rates impact investors?

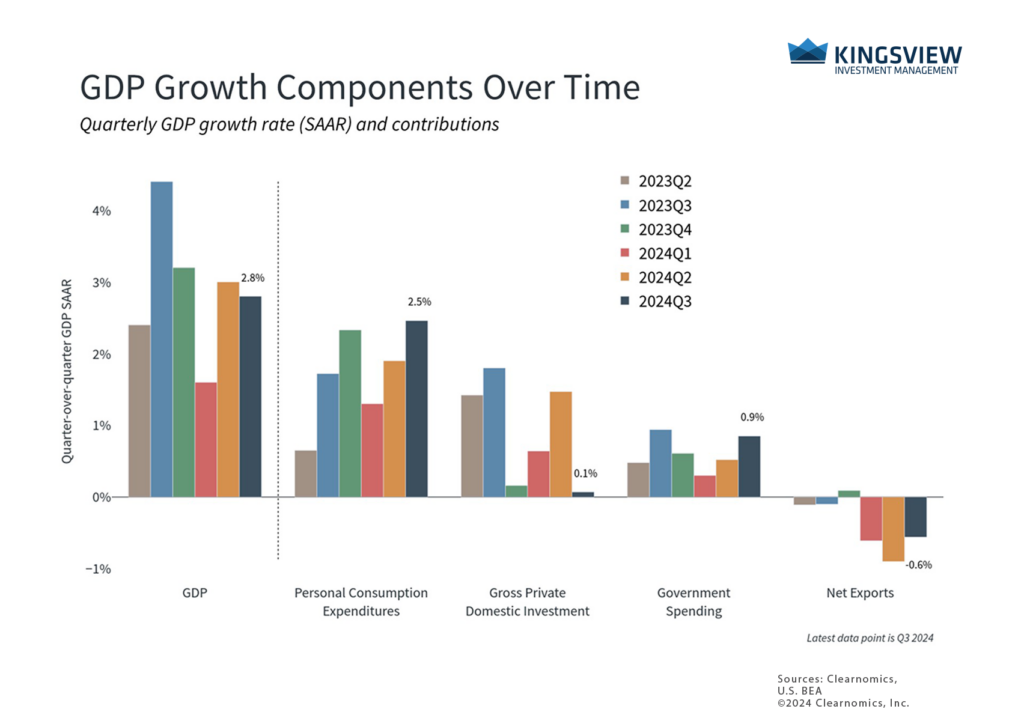

The economy continues to grow at a steady pace

Interest rates affect many parts of our lives, both directly and indirectly. Households are directly impacted when the cost of borrowing increases, which affects mortgages, credit cards, auto loans, and more. Many consumers experienced whiplash when borrowing costs jumped suddenly in 2022, after growing accustomed to ultra-low rates over the prior decade. On the flip side, rising interest rates can result in higher yields on bonds, savings accounts, certificates of deposit, money market funds, and more.

When it comes to the broader economy and financial markets, the effects can be more subtle. Higher rates increase the “cost of capital” for businesses, which can slow hiring, impede expansion plans, and reduce profitability. For the stock market, rising rates can theoretically reduce the value of future cash flows, reducing stock prices today. Higher rates can also make existing bonds less valuable, since newly issued bonds will offer higher yields. Thus, for investors, interest rates can have wide-ranging effects on portfolios.

What’s driving rates today? Unlike short-term rates which are influenced primarily by Federal Reserve policy, long-term interest rates are sensitive to economic trends. Fortunately, recent economic figures suggest the economy continues to grow at a steady pace. The latest GDP report showed that the economy grew 2.8% in the third quarter. While this was slightly below expectations, consumer spending remained exceptionally strong. Some economists worry this could reverse as consumers spend down their excess savings and debt levels rise.

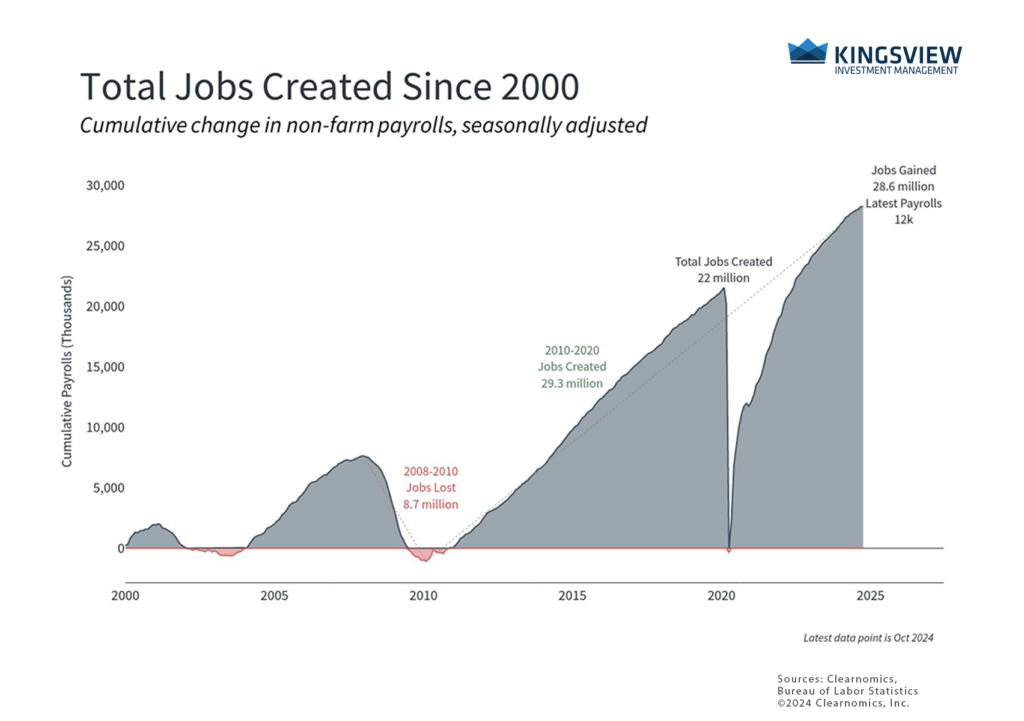

Recent jobs data have been more mixed. The jobs report immediately following the Fed’s September rate cut showed that 254,000 jobs were created that month, a blowout figure. This is one reason rates began to rise since a strong job market means the Fed may not need to cut rates as quickly to support the economy. In other words, the Fed could be achieving a so-called “soft landing” even with higher rates.

Job growth has slowed from a historically strong pace

However, the latest jobs numbers for October show that only 12,000 jobs were added last month – the lowest monthly figure since 2020. There were also significant downward revisions to prior months, lowering the September figure to 223,000. The Bureau of Labor Statistics cited strikes among manufacturing workers and the recent hurricanes in Florida as likely dampeners in the report, although the exact impact is difficult to determine from the survey data. For this reason, the market’s initial reaction was to look beyond this single data point.

The jobs numbers matter because they are of growing importance for Fed decision making. As inflation rates continue to fall back to more normal levels, hiring activity is what will affect households and everyday individuals.

Despite the recent poor data, the reality is that the job market has been exceptionally strong. Not only has the economy added 2.2 million new jobs over the past year, but the unemployment rate is only 4.1%. So, even if the economy does slow from here, it would be from an unusually healthy level.

Thus, rising long-term rates are not unusual if they are due to a stronger economy. In fact, it can be normal for short-term rates to fall as the Fed cuts rates even as long-term rates climb higher. In technical terms, this results in a “steepening yield curve,” which typically occurs in the early stages of economic cycles. While it’s unclear if this will continue this time, investors should not overreact to these patterns.

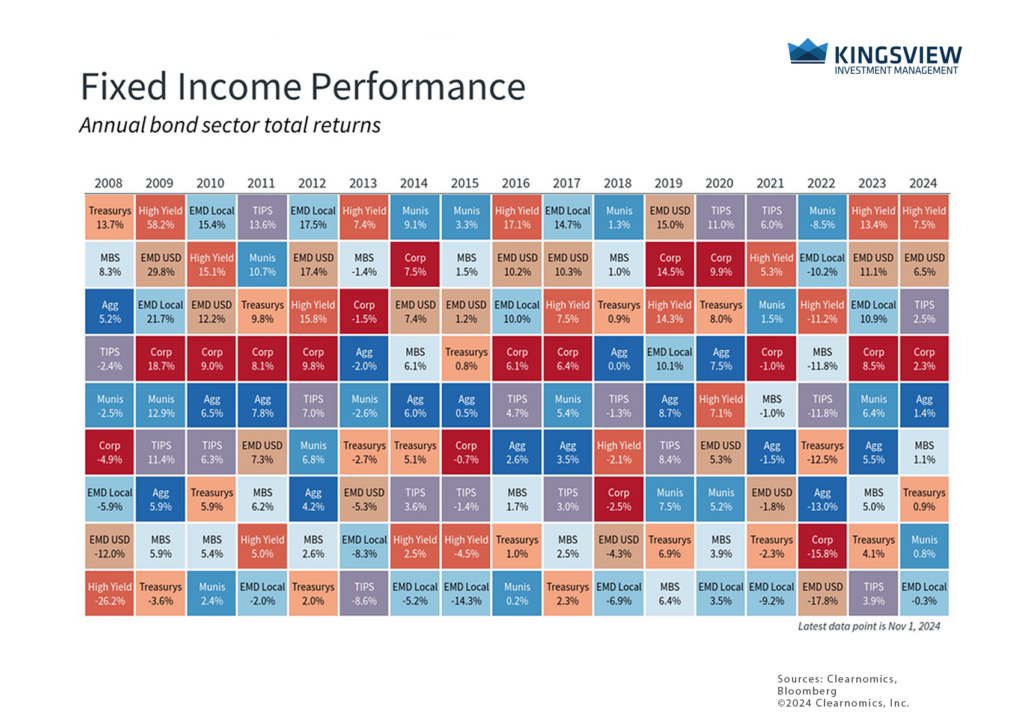

Bonds still support portfolios despite higher rates

Interest rate uncertainty has affected bond prices with the Bloomberg U.S. Aggregate index gaining only 1.4% year-to-date. Returns across sectors this year range from 7.5% for high yield bonds to only 0.8% for munis. This is because the prices of existing bonds fall as yields rise since newly issued bonds with higher yields become more attractive to investors.

However, these swings have taken place multiple times this year as markets have adjusted to different economic trends. Additionally, many of these bond sectors are offering yields well above their long run averages. The yields on Treasury bonds are 4.3%, well above the 2.0% average since 2009, and investment grade corporate bonds are yielding 5.2%.

For all investors, bonds still play an important role in not only diversifying portfolios during periods of uncertainty, but in providing income. As the chart above shows, returns by different types of bonds can vary greatly from year to year. While it’s not clear exactly where rates may go next, investors should maintain a longer-term perspective. It’s important to diversify properly across a variety of fixed income sectors to help weather market volatility.

The bottom line? Recent economic data, including a disappointing jobs report, may influence the Fed’s rate cut decisions. Investors should avoid overreacting to a single data point, and should instead stay diversified and maintain a longer-term perspective.